Grow Membership & Expand Lending with a Low-Income Designation

Data-Driven LID Support for Credit Unions

Why LID Matters More Then Ever

Running a credit union today means navigating a storm of challenges:

Business Lending Cap: Credit unions are restricted to a 12.25% cap on member business loans, limiting their ability to support local entrepreneurs.

Fixed Asset & PCA Rules: Regulations like the fixed asset cap and net worth requirements constrain growth and operations.

Missed Grants & FOM Growth: Without LID, credit unions lose access to financial grants and face challenges expanding into underserved areas.

But there’s a strategic solution that can give your credit union a real advantage:

A Low- Income Designation (LID)

An undeniable, competitive edge

Credit Unions with LID gain access to a host of benefits:

Lift the Member Business Loan Cap

Fuel local economic development without limits

Boost Net Worth with Subordinated Debt

Secondary capital counts toward your net worth ratio

Accept Non-Member Deposits

Raise funds from any source—up to the greater of $3M or 50% of your total shares

Access CDRLF Grants and Loans

Unlock technical assistance grants and low-cost loans through the NCUA

Grow Membership via Associational Paths

Federal community credit unions can add volunteers, association participants, and more

We deliver fast and informed LID results by combining proprietary software built with custom tools and deep subject matter expertise

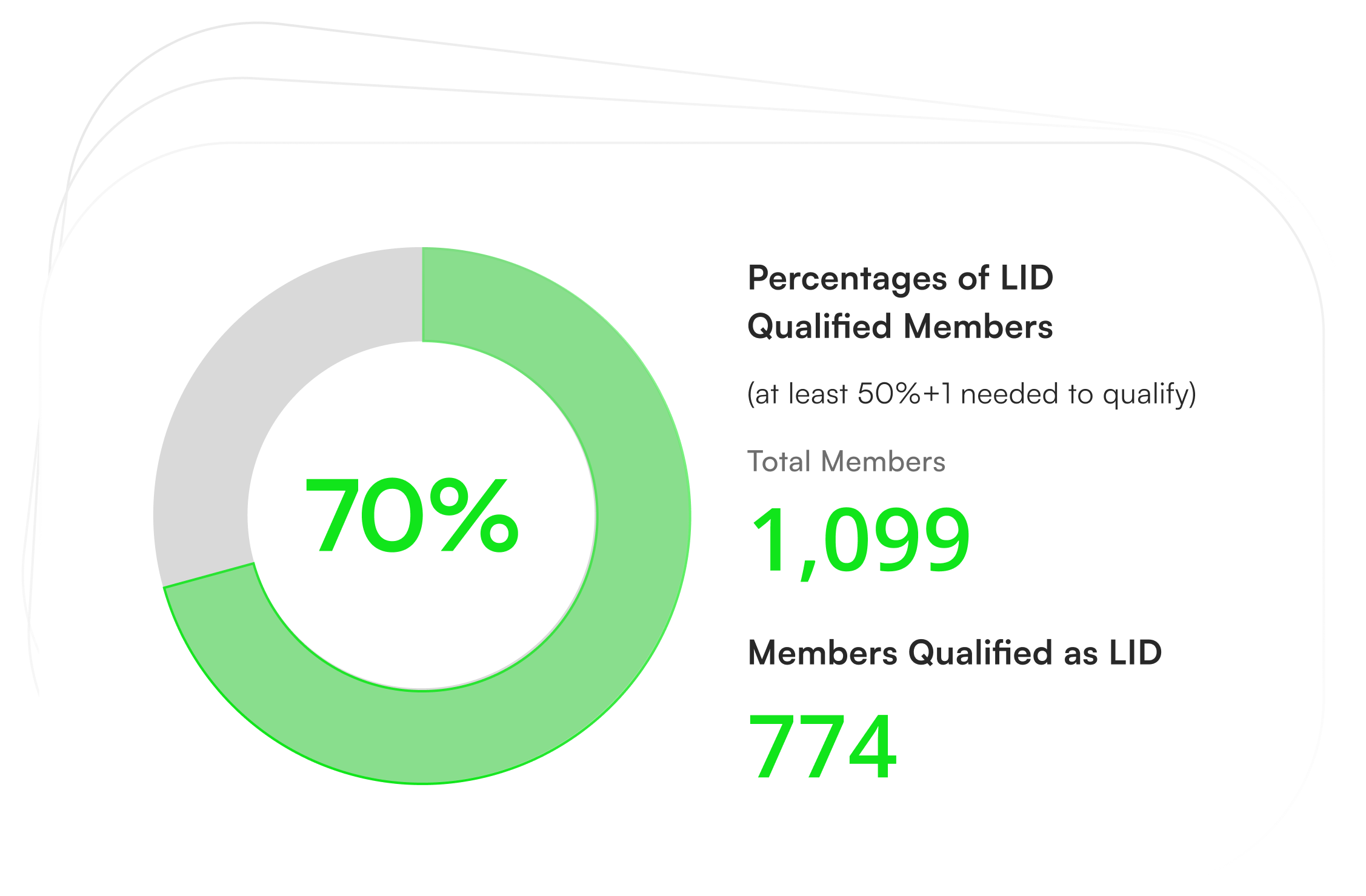

100%

success rate in LID

designations

100%

approval rate for securing secondary capital

46

active LID clients in

2024

CDRLF

funding secured for 12

credit unions

Three Routes to LID

Three Routes to LID

With our proven approach, any credit union can attain LID. We guide you through the path that makes the most strategic and practical sense for your institution.

Book Your LID Strategy Session

01/

AIRES Data

Analysis

The standard and most common route—match member data to LID geographies.

02/

Presumed Low-Income Community

Credit unions with community charters can use your FOM’s total potential membership to qualify.

03/

Loan Portfolio

Analysis

Demonstrate that the majority of your lending serves low-income borrowers.

Our Proven, Tech-Enabled Approach

We provide credit unions with a path to attain LID with certainty. And once you attain LID, we make it easier for you to keep it.

Book Your LID Strategy Session

Built to Help You Attain and Retain LID

Baseline Assessment: Review your current data and eligibility

Data Clean-Up & Enrichment

Identify data enrichment needed to maximize your current membership potential with qualifying individuals

Another Option for those with a Federal Community Charter

Easily build reports to demonstrate that a majority of the total potential membership meets the low-income definition.

For a Select Few, Loan Analysis is the Answer

Identify the % of Your Loans Issued to a Low-Income Target Population

Forward Flow Lending Partners

Our fintech lending partners leverage CUCollaborate’s proprietary LID & FOM APIs along with the credit union’s membership application and loan documentation to provide our clients with a consistent pipeline of new members and qualifying loans

Already have LID

We make it easier for you to retain your status through tracking and monitoring tools, including LID dashboards, APIs, and custom mapping tools.

Achieve More with the Power of LID

Regardless of where you are in your LID journey, we’ll help you use LID to fuel your mission, fund your growth, and serve your members better.